Mortgage rates below 5% are an historical anomaly. They only occurred because the Federal Reserve kept the fed funds rate abnormally low to fight off the 2008 financial crisis. It did so for 10 years, leading most of us to believe this was the new normal. Unless we see another global recession or a pandemic, it's unlikely we will see mortgage rates drop below 5% again.

Why 5% Mortgage Rates Are Abnormal

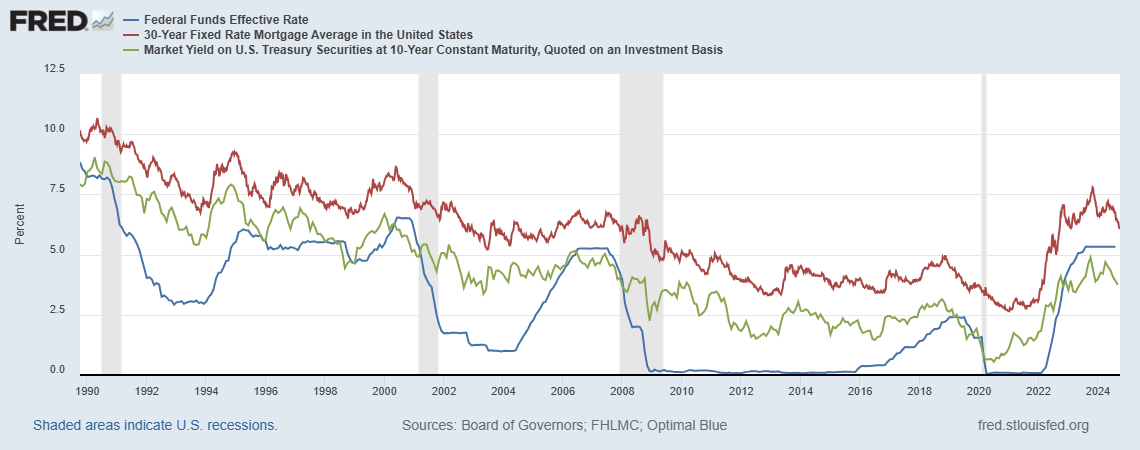

As the chart above shows, the 30-year fixed mortgage interest rate remained above 5% until the 2008 financial crisis (orange line at the top of the chart.)

The mortgage rate is usually around 2 percentage points above the yield on the 10-year U.S. Treasury note (green line in the middle.) The 10-year Treasury yield is usually higher than the Federal Reserve's fed funds rate. Investors want a higher return on long-term investments than on short-term ones.

As you can see, mortgage rates stayed above 5% until the financial crisis. Until then, the Fed kept its funds rate within its preferred 2-5% range. It only dropped the rate to zero to ward off financial collapse in 2008. The threat was so severe that it kept the rate that low for eight solid years. Mortgage rates stayed below 5% for a decade, long enough for most of us to believe that was the new normal.

How the Pandemic Messed Up Interest Rates

If the 2020 pandemic hadn't occurred, the Fed would have continued raising rates. You can see this in the chart, as the blue line rose between 2018 and 2020. The Fed prefers its rate to stay around 2%. You can see the 10-year Treasury yield and the 30-year mortgage interest rate started creeping up to more normal levels.

But when the pandemic hit in 2020, the Fed was forced to drop its rate back to zero. Treasury yields and mortgage rates also dropped. Then inflation skyrocketed in 2022. The Fed quickly increased its rate to 5.5%. As a result, mortgage rates rose to a 24-year high in October 2023.

What Happens Now?

By September 2024, inflation had cooled enough to allow the Fed to reverse course. It lowered the fed funds rate by 1/2 point to 5%.

How much lower will the rate go? The Fed's forecast told us. The Fed funds rate will fall another 1/2 point, to 4.5%, by the end of 2024. It will drop another full point, to 3.5%, by the end of 2025. That's high enough to keep mortgage rates above 5% for the next 18 months.

What It Means to You

Buyers: If you're lookin for the best rate, and that's all you care about, then waiting till the end of the year might be a good idea. On the other hand, inventory is usually at its lowest point, and you might not get the house you want. Furthermore, low inventory might also mean you'll have to pay a higher price. Will it offset the gains you make from lower interest rates? Do you want to take that chance?

Sellers: This could be a good time to sell, as there is not be a lot of competition. Research shows that 50% of homeowners have mortgage rates below 5%. They won't sell until rates fall below 5%. As a result, inventory is low, pushing prices higher. Find out now what your home is worth.